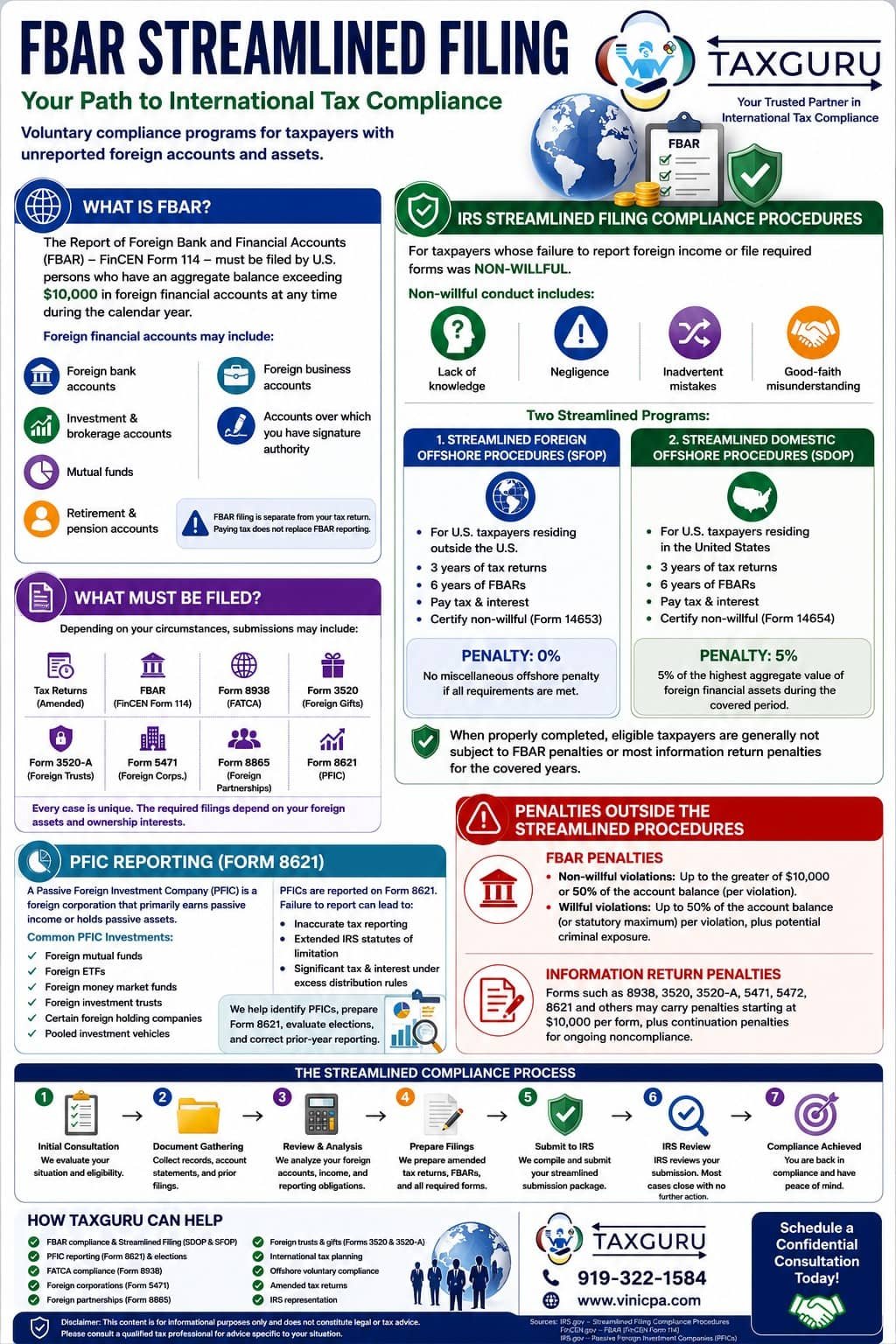

Have You Missed Reporting Foreign Bank Accounts?

Many U.S. taxpayers are surprised to learn that they must report foreign bank accounts, investment accounts, retirement accounts, and certain foreign financial assets—even if they have already paid taxes in another country.

If you recently discovered that you should have filed an FBAR (FinCEN Form 114), Form 8938, or other international information returns, don’t panic. The IRS offers the Streamlined Filing Compliance Procedures for eligible taxpayers whose failure to comply was non-willful.

This program allows many taxpayers to become compliant while significantly reducing or eliminating penalties.

What Is the FBAR?

The Report of Foreign Bank and Financial Accounts (FBAR), officially known as FinCEN Form 114, must generally be filed by U.S. persons who have an aggregate balance exceeding $10,000 in foreign financial accounts at any time during the calendar year.

Foreign financial accounts may include:

⦁ Foreign checking and savings accounts

⦁ Investment and brokerage accounts

⦁ Mutual funds

⦁ Certain pension and retirement accounts

⦁ Foreign business accounts

⦁ Accounts over which you have signature authority

Many taxpayers mistakenly assume that because they reported the income or paid foreign taxes, no additional reporting is required. Unfortunately, FBAR filing is a separate reporting requirement.

What Are the IRS Streamlined Filing Compliance Procedures?

The IRS created the Streamlined Filing Compliance Procedures for taxpayers whose failure to report foreign income or file required international forms resulted from non-willful conduct, such as:

⦁ Lack of knowledge of U.S. reporting requirements

⦁ Negligence

⦁ Inadvertent mistakes

⦁ Good-faith misunderstanding of complex international tax rules

The streamlined procedures are available only if the taxpayer certifies that the noncompliance was non-willful.

Two Types of Streamlined Programs

Unreported Foreign Accounts

Determine Eligibility

Streamlined Domestic / Foreign

IRS Compliance

1. Streamlined Foreign Offshore Procedures (SFOP)

Designed for eligible U.S. taxpayers who satisfy the IRS non-residency requirements.

Generally includes:

⦁ Three years of delinquent or amended federal tax returns

⦁ Six years of FBAR filings

⦁ Payment of any tax and interest due

⦁ Certification of non-willful conduct (Form 14653)

Penalty

0% miscellaneous offshore penalty

Eligible taxpayers generally avoid FBAR penalties and other information return penalties when all program requirements are satisfied.

2. Streamlined Domestic Offshore Procedures (SDOP)

Designed for taxpayers residing in the United States who qualify under the IRS eligibility rules.

Generally requires:

⦁ Three years of amended federal tax returns

⦁ Six years of FBAR filings

⦁ Payment of additional tax and interest

⦁ Certification of non-willful conduct (Form 14654)

Penalty

A 5% miscellaneous offshore penalty applies to the highest aggregate year-end balance/value of certain foreign financial assets subject to the penalty during the covered period. When properly completed, eligible taxpayers are generally not subject to separate FBAR penalties or most international information return penalties for the covered years.

What Must Be Filed?

Depending on your situation, the submission may include:

⦁ Amended federal income tax returns

⦁ FBARs (FinCEN Form 114)

⦁ Form 8938

⦁ Form 3520

⦁ Form 3520-A

⦁ Form 5471

⦁ Form 5472

⦁ Form 8621 (PFIC)

⦁ Form 8865

⦁ Form 926

⦁ Other required international information returns

Every case is unique, and the required filings depend on your foreign assets and ownership interests.

Penalties Outside the Streamlined Procedures

Failure to comply with international reporting requirements can result in substantial civil penalties.

Potential penalties may include:

FBAR Penalties

⦁ Non-willful violations – The IRS may assess civil penalties for non-willful violations, subject to statutory limits and inflation adjustments, if relief is unavailable.

⦁ Willful violations – Willful FBAR violations may result in penalties of up to 50% of the account balance (or the applicable statutory maximum) for each violation, in addition to potential criminal exposure in severe cases.

International Information Return Penalties

Numerous IRS information returns carry separate penalties, including:

⦁ Form 5471

⦁ Form 5472

⦁ Form 3520

⦁ Form 3520-A

⦁ Form 8938

⦁ Form 8621

These penalties may begin at $10,000 per form, with additional continuation penalties possible if the failure is not corrected after IRS notification. The exact amount depends on the specific form and circumstances.

Who Qualifies?

The streamlined procedures are intended for taxpayers who:

⦁ Failed to report foreign income or assets

⦁ Failed to file FBARs or required international information returns

⦁ Were not willful

⦁ Are not currently under IRS civil examination or criminal investigation

⦁ Meet the IRS residency and eligibility requirements for either the domestic or foreign streamlined program

Why Timing Matters

Many taxpayers discover their filing obligations only after:

⦁ Receiving FATCA reporting notices from foreign banks

⦁ Applying for U.S. citizenship documentation

⦁ Selling foreign investments

⦁ Receiving inherited foreign assets

⦁ Working with a new CPA

Waiting too long can reduce available compliance options if the IRS contacts you first.

How Jain Consulting Can Help

International tax compliance requires careful planning and technical expertise. At Jain Consulting, we assist clients throughout the United States and abroad with:

⦁ FBAR compliance

⦁ Streamlined Domestic Offshore Procedures

⦁ Streamlined Foreign Offshore Procedures

⦁ PFIC (Form 8621) reporting

⦁ FATCA (Form 8938)

⦁ Foreign corporations (Form 5471)

⦁ Foreign partnerships (Form 8865)

⦁ Foreign trusts and gifts (Forms 3520 and 3520-A)

⦁ International tax planning

⦁ Offshore voluntary compliance

⦁ Amended tax returns

⦁ IRS representation

Our team works with individuals, business owners, expatriates, investors, and taxpayers with inherited foreign assets to develop a compliance strategy tailored to their circumstances.

Schedule a Confidential Consultation

If you have unreported foreign bank accounts, foreign investments, inherited overseas assets, or missed FBAR filings, it is important to evaluate your options before the IRS contacts you.

The sooner you address the issue, the more compliance options may be available.

Contact Jain Consulting today to discuss your international tax compliance needs. Our experienced professionals can evaluate your eligibility for the IRS Streamlined Filing Compliance Procedures and help you navigate the filing process with confidence.

Disclaimer: This article is provided for informational purposes only and does not constitute legal or tax advice. Every taxpayer’s situation is unique. Professional advice should be obtained before taking action.