U.S. Tax impact for the Sale of Foreign Real Estate

The sale of foreign real estate by U.S. taxpayers involves several intricate tax considerations under U.S. tax law. This article will explore how such sales are treated, the reporting requirements, the application of the Foreign Tax Credit (FTC), the impact of currency exchange rates, the treatment of capital gains, relevant tax treaties, and the implications of the Foreign Account Tax Compliance Act (FATCA) and the Foreign Bank and Financial Accounts (FBAR) form.

Treatment of the Sale of Foreign Real Estate Under U.S. Tax Law

Under U.S. tax law, the sale of foreign real estate by a U.S. taxpayer is treated similarly to the sale of domestic real estate. The taxpayer must report the sale on their U.S. tax return and calculate the gain or loss from the sale. The gain or loss is determined by subtracting the adjusted basis of the property (original purchase price plus improvements and less depreciation, if applicable) from the amount realized on the sale (sale price minus selling expenses).

Reporting Requirements for U.S. Taxpayers

U.S. taxpayers must report the sale of foreign real estate on Form 1040, Schedule D (Capital Gains and Losses), and Form 8949 (Sales and Other Dispositions of Capital Assets). If the property was used for business or rental purposes, the sale must also be reported on Form 4797 (Sales of Business Property).

Application of the Foreign Tax Credit (FTC)

To mitigate double taxation, U.S. taxpayers can claim a Foreign Tax Credit (FTC) for foreign taxes paid on the sale of the real estate. The FTC is claimed on Form 1116 (Foreign Tax Credit). The credit is limited to the lesser of the foreign taxes paid or the U.S. tax liability on the foreign-source income. This ensures that the taxpayer does not pay more tax than they would have if the income were earned in the U.S.

Impact of Currency Exchange Rates on the Calculation of Gain or Loss

The gain or loss from the sale of foreign real estate must be calculated in U.S. dollars. This involves converting the purchase price, improvements, selling expenses, and sale proceeds from the foreign currency to U.S. dollars using the exchange rates in effect on the respective dates of the transactions. Fluctuations in exchange rates can significantly impact the reported gain or loss.

Treatment of Capital Gains and Applicable Tax Rates

Capital gains from the sale of foreign real estate are generally treated as long-term or short-term capital gains, depending on the holding period of the property. If the property was held for more than one year, the gain is considered long-term and is subject to preferential tax rates of 0%, 15%, or 20%, depending on the taxpayer’s income level. Short-term capital gains, for property held one year or less, are taxed at ordinary income tax rates.

Relevant Tax Treaties

Tax treaties between the U.S. and other countries can affect the taxation of the sale of foreign real estate. These treaties often provide relief from double taxation and may allow for the deferral of U.S. tax until the foreign tax is paid. Taxpayers should consult the specific tax treaty between the U.S. and the country where the property is located to determine the applicable provisions.

Implications of FATCA and Form 8938

The Foreign Account Tax Compliance Act (FATCA) requires U.S. taxpayers to report foreign financial assets, including foreign real estate held through a foreign entity, on Form 8938 (Statement of Specified Foreign Financial Assets). This form is filed with the taxpayer’s annual tax return if the total value of the foreign assets exceeds certain thresholds ($50,000 on the last day of the tax year or $75,000 at any time during the tax year for single filers; higher thresholds apply for married taxpayers filing jointly).

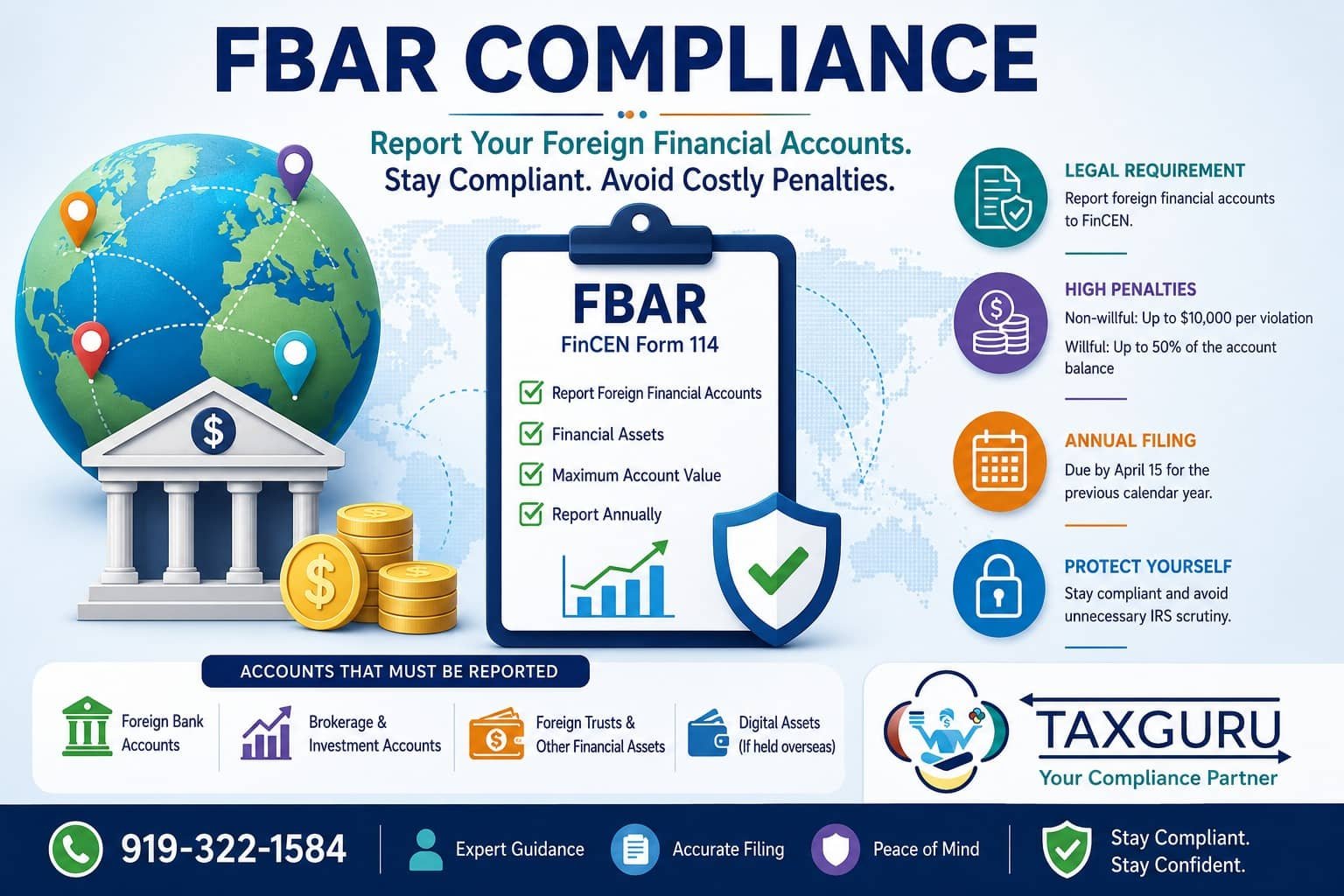

Requirement to Report on FBAR

If the foreign real estate is held through a foreign bank account or other financial account, the taxpayer may also need to report the account on the Foreign Bank and Financial Accounts (FBAR) form, FinCEN Form 114. The FBAR must be filed if the aggregate value of all foreign financial accounts exceeds $10,000 at any time during the calendar year.

Conclusion

The sale of foreign real estate by U.S. taxpayers involves complex tax considerations, including reporting requirements, the application of the Foreign Tax Credit, the impact of currency exchange rates, and the treatment of capital gains. Taxpayers must also be aware of the implications of FATCA and the requirement to report foreign financial assets on Form 8938 and the FBAR form. Consulting with a tax professional familiar with international tax issues is advisable to ensure compliance and optimize tax outcomes.

Author of this article Jack Chaudhary specializes in Individual, Corporate Tax returns, Foreign Taxes, Expats, Non-resident Taxes, Payroll, Crypto and e-Commerce. With the Enrolled Agent credential, Jack represents taxpayers before the IRS and state taxing authorities. He zealously advocates for his clients to ensure the best results are achieved. Book an appointment here with him for a consultation call.