How are foreign pension funds taxed for US citizens ?

Foreign pension funds are subject to complex tax rules for U.S. citizens, encompassing the tax treatment of contributions, earnings, and distributions, as well as the impact of tax treaties and reporting requirements. This article provides a comprehensive overview of these aspects, drawing on relevant sections of the Internal Revenue Code (IRC) and Treasury Regulations.

Tax Treatment of Contributions

Contributions to Exempt Trusts

For U.S. tax purposes, contributions to foreign pension funds that do not qualify as exempt trusts under IRC § 401(a) and are not exempt from tax under IRC § 501(a) are generally included in the gross income of the employee in accordance with IRC § 83. Specifically, IRC § 402(b)(1) states that contributions made by an employer to a nonexempt employees’ trust are included in the employee’s gross income when the employee’s interest in the trust becomes substantially vested [1].

Contributions to Nonexempt Trusts

If the foreign pension fund is treated as a nonexempt employees’ trust, the contributions are taxed under IRC § 402(b). Contributions made by the employer are included in the employee’s gross income when they become vested, as per IRC § 83. The value of the employee’s interest in the trust is substituted for the fair market value of the property for purposes of applying IRC § 83 [1].

Tax Treatment of Earnings

Earnings in Exempt Trusts

Earnings within a foreign pension fund that qualifies as an exempt trust under IRC § 401(a) and is exempt from tax under IRC § 501(a) are generally not taxed until distributed. This deferral of tax on earnings is a significant benefit of qualifying as an exempt trust [1].

Earnings in Nonexempt Trusts

For nonexempt employees’ trusts, earnings are generally includable in the employee’s gross income when distributed or made available, as per IRC § 402(b)(2). However, if the trust is discriminatory and fails to meet the requirements of IRC § 410(b), highly compensated employees may have to include the vested accrued benefit in their gross income annually [1].

Tax Treatment of Distributions

Distributions from Exempt Trusts

Distributions from an exempt trust are generally taxed under IRC § 72, which deals with annuities. The amount distributed is included in the gross income of the distributee in the year it is distributed [1].

Distributions from Nonexempt Trusts

Distributions from nonexempt employees’ trusts are also taxed under IRC § 72. However, distributions of income from the trust before the annuity starting date are included in the gross income of the employee without regard to IRC § 72(e)(5) [1].

Relevant Tax Treaties

Tax treaties can significantly affect the taxation of foreign pension funds. For instance, the U.S.-U.K. tax treaty provides that distributions from U.K.-based pension plans to U.S. residents are generally taxable only in the United States. The treaty also allows for certain amounts to be received tax-free if they would be exempt from tax in the U.K. [4].

Reporting Requirements

Form 3520 and Form 3520-A

U.S. persons with interests in foreign trusts, including foreign pension funds treated as trusts, must file Form 3520 and Form 3520-A. These forms report transactions with foreign trusts and the receipt of certain foreign gifts [6].

Form 8938

Specified foreign financial assets, including interests in foreign pension funds, must be reported on Form 8938 if the total value exceeds certain thresholds. This form is filed with the taxpayer’s annual income tax return [6].

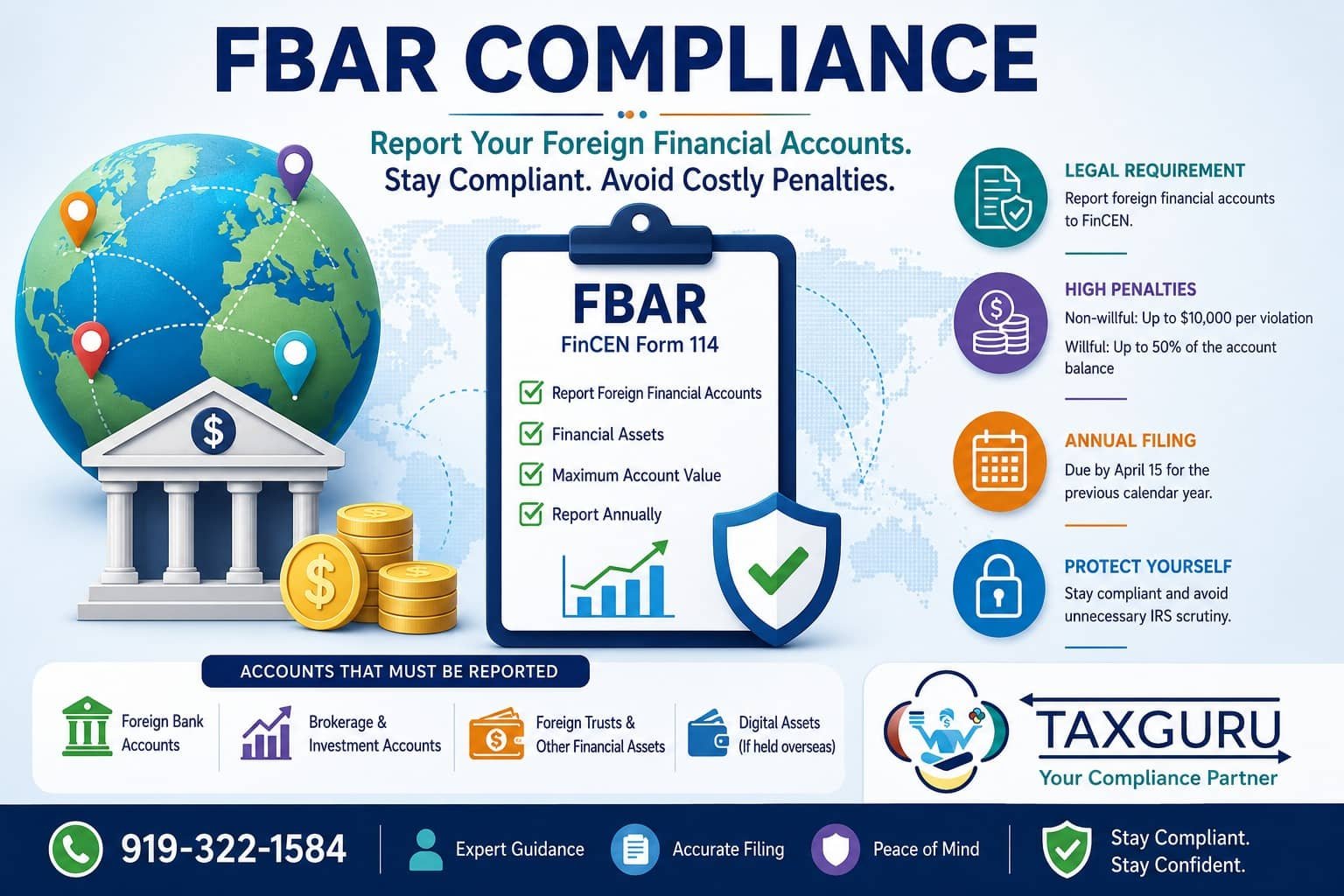

FBAR (FinCEN Form 114)

U.S. persons with a financial interest in or signature authority over foreign financial accounts, including foreign pension funds, must file an FBAR if the aggregate value of the accounts exceeds $10,000 at any time during the calendar year [6].

Conclusion

The taxation of foreign pension funds for U.S. citizens involves intricate rules regarding contributions, earnings, and distributions. Tax treaties can provide relief and modify the general tax treatment, but compliance with reporting requirements is crucial to avoid significant penalties. Understanding these rules and seeking professional advice is essential for U.S. citizens with interests in foreign pension funds.

Author of this article Jack Chaudhary specializes in Individual, Corporate Tax returns, Foreign Taxes, Expats, Non-resident Taxes, Payroll, Crypto and e-Commerce. With the Enrolled Agent credential, Jack represents taxpayers before the IRS and state taxing authorities. He zealously advocates for his clients to ensure the best results are achieved. Book an appointment here with him for a consultation call.