When U.S. Citizens Inherit from Non-Resident Parents: Navigating the Tax Landscape

Inheriting assets from non-resident parents can be a complex process for U.S. citizens, involving a myriad of tax implications and legal requirements. Understanding these intricacies is crucial to ensure compliance with U.S. tax laws and to optimize the financial benefits of the inheritance. This article delves into the key considerations and steps U.S. citizens should take when inheriting from non-resident parents.

Understanding U.S. Estate and Gift Tax Rules

The U.S. tax system imposes estate and gift taxes on the worldwide assets of U.S. citizens and residents. However, non-resident aliens (NRAs) are subject to U.S. estate tax only on their U.S.-situs assets. These include real estate and tangible personal property located in the United States, shares of U.S. corporations, and certain debt obligations of U.S. persons.

Estate Tax Exemption for Non-Residents

Non-resident decedents are granted a limited estate tax exemption of $60,000 for their U.S.-situs assets. Any value exceeding this threshold is subject to U.S. estate tax, which can reach up to 40% for estates valued over $1 million. This exemption is significantly lower than the $12.92 million exemption available to U.S. citizens and residents in 2023.

Transfer Certificates and U.S. Bank Accounts

To transfer U.S.-situs assets from a non-resident decedent, a transfer certificate from the IRS is often required. This certificate assures that any applicable U.S. estate taxes have been paid or that no tax is due. Without this certificate, U.S. financial institutions may freeze the decedent’s assets to avoid potential liability for unpaid estate taxes.

Obtaining a Transfer Certificate

To obtain a transfer certificate, the executor or heir must submit Form 706-NA, “United States Estate (and Generation-Skipping Transfer) Tax Return (Estate of Nonresident Not a Citizen of the United States),” along with supporting documents. These documents typically include:

- A copy of the decedent’s will and any codicils.

- Death certificates.

- A detailed list of the decedent’s U.S.-situs assets and their values at the date of death.

- Any foreign death tax or inheritance tax returns filed.

The IRS generally processes these requests within six to nine months.

Income Tax Considerations

Inheriting assets from non-resident parents can also have income tax implications. U.S. citizens must report and pay taxes on any income generated by the inherited assets. This includes dividends, interest, and rental income from U.S.-situs properties.

Basis Step-Up

One significant benefit for heirs is the step-up in basis for inherited property. Under IRC Section 1014, the basis of inherited property is generally stepped up to its fair market value at the date of the decedent’s death. This step-up can significantly reduce capital gains taxes if the property is later sold. However, the application of this rule can be complex when dealing with foreign estates, especially if the property is not included in the decedent’s U.S. taxable estate.

Reporting Requirements

U.S. citizens inheriting from non-resident parents must comply with various reporting requirements to avoid penalties. Key forms include:

- Form 3520: This form is used to report the receipt of large gifts or bequests from foreign persons. Failure to file can result in significant penalties.

- Form 8938: This form is required for reporting specified foreign financial assets if the total value exceeds certain thresholds.

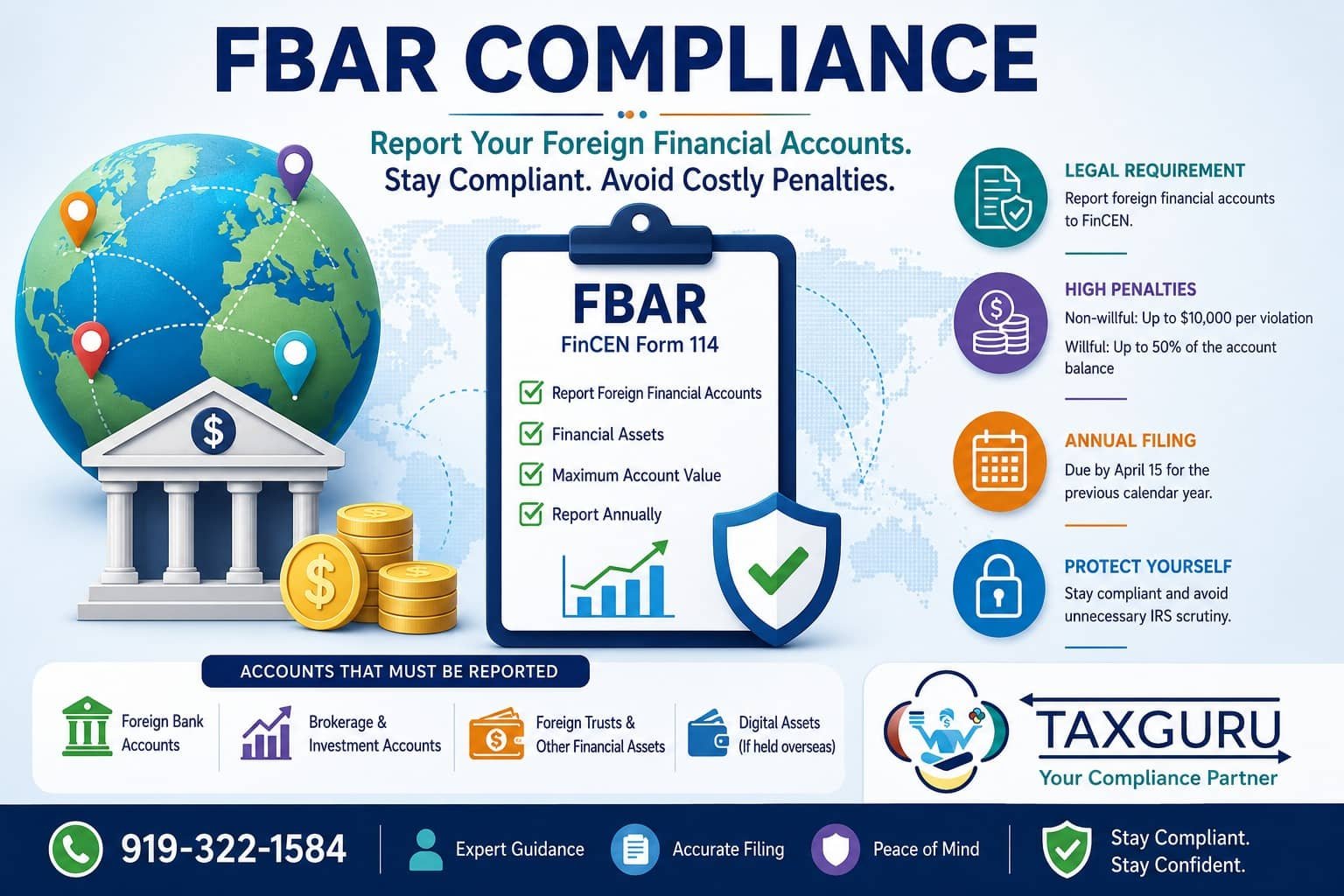

- FBAR (FinCEN Form 114): U.S. persons must file an FBAR if they have a financial interest in or signature authority over foreign financial accounts exceeding $10,000 in aggregate value at any time during the calendar year.

Estate Planning Strategies

To minimize U.S. tax liabilities, non-resident parents can employ various estate planning strategies. These may include:

- Gifting Assets During Lifetime: Non-resident parents can gift assets to their U.S. children during their lifetime, taking advantage of the annual gift tax exclusion ($17,000 per recipient in 2023). Gifts of intangible assets, such as stocks in non-U.S. corporations, are not subject to U.S. gift tax.

- Using Foreign Trusts: Establishing a foreign trust can provide tax benefits and asset protection. However, the trust must be carefully structured to comply with U.S. tax laws and avoid adverse tax consequences for the U.S. beneficiaries.

- Life Insurance: Proceeds from life insurance policies are generally not subject to U.S. estate tax, making them an effective tool for transferring wealth.

Conclusion

Inheriting from non-resident parents involves navigating a complex web of U.S. tax laws and reporting requirements. U.S. citizens should seek the guidance of experienced tax professionals to ensure compliance and optimize their financial outcomes. Proper planning and understanding of the relevant tax rules can help mitigate potential tax liabilities and ensure a smooth transfer of assets.

Author of this article Jack Chaudhary specializes in Individual, Corporate Tax returns, Foreign Taxes, Expats, Non-resident Taxes, Payroll, Crypto and e-Commerce. With the Enrolled Agent credential, Jack represents taxpayers before the IRS and state taxing authorities. He zealously advocates for his clients to ensure the best results are achieved. Book an appointment here with him for a consultation call.